Tourism What Is a Destination Sentiment Monitor? A Plain-English Guide for Destination Managers A Destination Sentiment Monitor continuously analyses publicly available conversations from travel reviews, news articles, blogs, forums, and social media to help destinations understand how they are perceived. I

Beyond Dashboards: Why Every Destination Needs an AI Sentiment Observatory The future of destination marketing isn't just about measuring visitor numbers—it's about understanding how people feel before they book.

How to Read Air Arrival Data A practical guide for tourism professionals who want to understand what air-arrival numbers actually mean.

Tourism Top 10 Tourism Data Mistakes DMOs Make Tourism decisions are often based on historical reports, fragmented datasets, or assumptions rather than evidence. The result is missed opportunities, inefficient marketing, and weaker investment decisions.

Tourism Featured STATE OF THE WORLD 2026 Tourism Strategy 2026: Navigating the Future of Global Travel

Tourism The Season That Isn't: Rerouting Tourism When the Seasons Shift As climate change collapses traditional tourism seasons, DMOs and small operators must rethink peak travel calendars. This guide covers heatwave-driven coolcation trends, shifting monsoons in Southeast Asia, and practical strategies for destination-level demand design and small-operator revenue dive

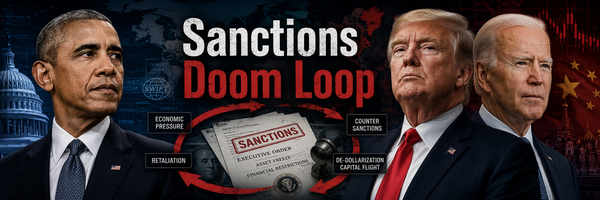

Economics The Machine That Cannot Stop:A Systems Analysis of US Sanctions The US sanctions regime is a self-reinforcing machine eating its own foundation. We map the feedback loops, hidden costs, and de-dollarisation trendline that will determine whether the system survives the 2030s.

The Cambodia Scam Bill and the Expanding U.S. Sanctions Machine U.S. sanctions are expanding from wartime tools into a global financial weapon. This analysis explains the Cambodia scam bill, Sar Sokha’s legal response, OFAC, SDN designations, dollar power, due process concerns, and what it means for Cambodia.

Cambodia Cambodia's Capital Gains Tax -Why Now Isn't the Right Time Cambodia’s 20 % Capital Gains Tax, slated for 2025-26, risks adding red tape, spooking foreign investors, and prolonging the real-estate slump. Explore why timing, fairness and administrative capacity make CGT the wrong tool for Cambodia’s fragile recovery.

Tourism AI Is Rewriting the Tourism Map — Will Your Destination Be on It? AI is transforming travel planning by shaping what travelers see, book, and experience. Destinations must now optimize digital content, branding, and visibility to stay relevant. Learn how to future-proof your tourism business in the era of AI-driven travel.

Tourism The Airbnb of 2040: Emergent Systems, Economic Rethinks, and the Next Travel Revolution Explore how tourism accommodation could evolve beyond Airbnb by embracing emergent complexity theory. Discover future-ready, adaptive models that prioritize sustainability, decentralization, and AI-driven matchmaking in the travel industry of 2040.

Tourism Data-driven Approaches for Small Operators in Tourism and Experiential Tours Unlock growth with a data-driven approach! Dive into SEO and social media strategies tailored for small businesses. Boost visibility and engage effectively.

Tourism Destination Sentiment Analysis GPT Discover how the Destination Sentiment Analysis GPT revolutionizes travel marketing by enabling small operators to analyze traveler sentiment at scale. Learn how this AI tool helps craft targeted messaging that outperforms competitors through data-driven insights.

Cambodia Cambodia's Demographic Dividend Slipping Through Our Fingers Cambodia's demographic dividend is rapidly fading due to structural economic barriers including dollarization, outmigration, and poor digital infrastructure. This analysis explores critical challenges and pragmatic solutions for harnessing Cambodia's youth population before the opportunity lost.

Tourism DMO AI Toolkit - Transform Tourism with a Cutting-Edge AI Solution for Destination Development and Management Discover an AI tool tailored for DMOs and small operators, offering strategic tourism insights, sustainable marketing solutions, and data-driven strategies. From niche product development to crisis management, empower your destination to thrive in today’s competitive tourism landscape.

Tourism Part I: Destination Management 2025 - Destination Fees & Taxes Discover how high tourism taxes and fees can harm destination competitiveness in 2025. Learn from case studies of destinations that thrived with transparency and those that struggled due to overpricing. Stay ahead with strategies for balancing sustainability, affordability, and traveler satisfaction

Cambodia Cambodia's Digital Transformation: A Bold Vision for an AI-Powered Future Discover Cambodia's bold leap into AI with a cutting-edge data center vision. Learn how this transformative project drives technological innovation, lures foreign investment, and sparks sustainable growth—fueling the kingdom’s future in travel and beyond.

Tourism Marketing Tourism During Periods of Unrest: Strategies for Success Discover effective strategies for marketing tourism during periods of unrest. Learn from Cambodia, Kenya, New Zealand, and Vietnam's experiences.

Tourism How War and Conflict Change Perceptions: A Guide for Policy and Destination Planners Discover how war and conflict reshape tourism, influencing perceptions and guiding destinations to brand themselves as safe havens.

Tourism Understanding Generative Search and Its Impact on Tourism Understanding Generative Search and Its Impact on Tourism Generative search is an advanced form of search technology that uses artificial intelligence (AI) to understand and generate human-like text based on user queries. Unlike traditional search engines that rely on keyword matching, generative search comprehends the context and nuances of

Tourism How is Generative Search Expected to Impact Traditional SEO Explore how generative search transforms SEO by enhancing user query understanding and content customization, shaping future SEO strategies.

Tourism Embracing Sustainability in Tourism: A Path to Eco-Friendly Growth and Conservation Explore sustainable tourism practices for eco-friendly growth, aligning with SDGs and balancing conservation with tourism development.

Tourism MICE: DMO Success Stories Aided by AI Explore key strategies for DMOs/NTAs in MICE market development: infrastructure, marketing, partnerships, and case studies of Dubai & Saudi Arabia.

Tourism Empowering Small Operators in Destinations Without DMO Support Through AI Custom chat GPTs for tourism for the small operator. For social media, websites, and personalized rural tours. Consulting available.

Tourism Sustainable Journeys: Crafting Unique Rural and Urban Adventures for the Conscious Traveler Explore the dynamic world of sustainable travel! Dive into rural tourism, culinary fun, and community-centric adventures for a unique and rewarding journeys.